Executive summary

- We have upgraded our Asia ex-Japan and China equity view to bullish from positive.

- Our broader 3i’s investment themes of Industry 5.0 and Innovation have positive spillover impacts for our positioning in Asia – namely in the AI-related space (like chip manufacturing) and other high-end value added activities.

- China’s comprehensive stimulus measures raises our conviction in Asia ex-Japan and China equities.

- Earnings growth in Asia is on an uptrend and well supported, with favourable contributions from India, Taiwan and South Korea – underpinned by rising global demand across new industrials, tech, and high-end value-added manufacturing.

- The outlook for Asia’s corporates is further reinforced from improved competitiveness, stronger supply-chain activities, and robust US consumerism.

- Most of our portfolios including our global strategies, have elevated positions in China and the leading chip manufactures of Asia.

- We are also invested in trends underpinned by longer-term supportive tailwinds – like “AI and associated infrastructure” as well as the “Survival of the fittest” theme.

Bullish 12-month view on Asia ex-Japan equities within the wider framework of our 3i’s investment theme

Our 3i’s investment theme comprises of Industry 5.0, Innovation, and Involution. We see these three key structural forces shaping the longer-term direction of global markets going forward. The world is at the cusp of Industry 5.0, which is the latest technology-led development driving gains in the AI and metaverse-related sectors. Advances in these areas underpinned by rising innovation, can further boost productivity, lower costs, and result in better products and increased spending – lifting earnings and profitability in the process for related players in this space, and across the broader economy. This presents newfound opportunities for selected industries – like the Asian semiconductor manufacturers for example, which are developing chips extensively used in the fields of AI and other high-end value-added activities.

These innovation-led gains are nonetheless taking place amidst the backdrop of ongoing headwinds in China – as policymakers search for solutions to address challenges across the real-estate sector, resolve economic-wide deflation, rebalance more toward consumption spending, and boost corporate performance. The involution theme reflects the Chinese administration’s adoption of more inward-looking strategies to tackling these issues.

Increased conviction in Asia ex-Japan and China equities: Involution is evolving

China’s involution is evolving. In our end-July Q3 Fullerton Investment View we moved to a positive view on China equities, harmonising with our positive outlook for Asia (ex-Japan) equities (held since January), as China’s earnings growth expectations improved with the most acute deflation past. Now into Q4 China’s policymakers have surprised markets by announcing the most significant monetary and fiscal stimulus plans since the Covid pandemic. These new initiatives are certainly the necessary conditions for China to be in a position that it may finally reverse producer-price deflation and boost corporate profitability over time.

China’s new policy stimulus plans present the best chance of success because they are multi-pronged across both the monetary and fiscal fronts, and very targeted at addressing the key areas of deflation risk (especially across the real-estate sector and consumer spending). In addition, there may now be far too much credibility at stake, from President Xi Jinping down to the province-level officials, for ‘policy failure’ to be acceptable.

To recap, the key objective of the monetary policy stimulus is to boost liquidity (to support investor sentiment), encourage more bank lending (to firms and households) and boost housing demand. The People’s Bank of China (PBoC) has used all its tools, from Reserve Requirement Ratio (RRR) and policy rate cuts to release longer-term liquidity in the banking sector, and ease the debt servicing burden on outstanding mortgages. There were also housing policy relaxation actions to reduce the minimum downpayments for second home purchases (lowered to 15% from 25% previously1), and other home-buyer financial supports (which should help demand for real estate stabilise and slowly improve over time). The PBoC will also allow securities firms, funds, and insurance companies, to tap its funding to buy equities (including their own shares, in a swap agreement). A separate specialised re-lending facility will also be established for listed companies and major shareholders to buy back their own shares. Collectively, these measures2 are expected to further lift investor sentiment over time.

For its new fiscal policy stimulus, China has confirmed it will increase government debt significantly with spending targeted to support households, the real-estate sector, along with the banks (to free-up capital for more lending), and with more resources channelled toward local government spending programmes. Around 2-3tn CNY in debt-raised funds will be deployed by year-end, with an (initial) issuance cap (into 2025) of up to 6tn CNY3. Tax cuts have also been rumoured and we will have to wait until the NPC meeting around the end of the month for any more details.

We now have a stronger conviction that equity markets in Asia can potentially deliver robust returns over our forecast horizon into 2025, and have revised our outlook up from positive to bullish – for both China and Asia ex Japan equities.

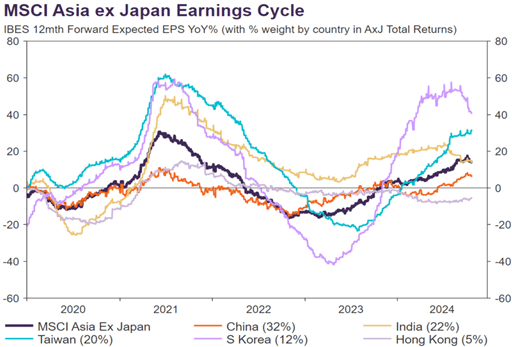

Asia ex Japan aggregate earnings growth expectations are high (i.e now 1 standard-deviation above the 10y average) with favourable contributions from India, Taiwan and South Korea (see Figure 1). The latter two markets are heavily linked to the positive spillover effects from Industry 5.0, benefitting from increased global demand across new industrials, the tech sector, and high-value added manufacturing. The chip manufacturers, in particular stand to benefit strongly. China’s earnings growth expectations have also given an added boost, and this may get further support as the impacts from the new stimulus unfold – especially in boosting consumption. Across Asia, corporates should continue to benefit from improved competitiveness, stronger supply-chain activities, and robust US consumerism demands.

Figure 1: Strong earnings growth for Asia and China is returning

Source: LSEG Datastream, October 2024.

Shock and awe policy announcements are always tricky for markets to “price-in” effectively – they will overshoot in the near-term, and it will be volatile. But so far, investors seem confident on real-estate stabilising, and banks performing well. In such an environment, value stocks and consumer-linked equities could hold up. The latter will be a key barometer sector because stronger household spending, and credit demand, will be critical to any sustainable recovery.

Implications for portfolio positioning

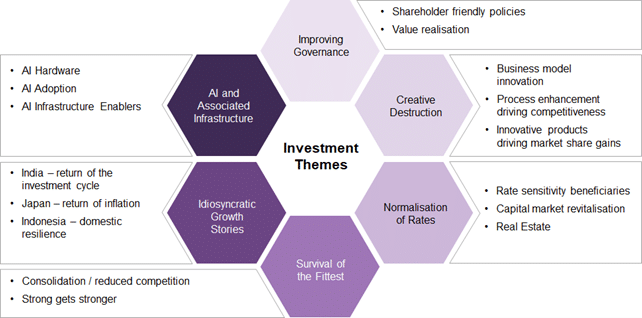

Given our bullish view on Asia ex-Japan equities and China (specifically in areas linked to some of the broader 3i’s themes of “Industry 5.0” and “Innovation”), it should come as little surprise that most of our portfolios including our global strategies, have elevated positions in China, and the leading chip manufactures of Asia. Beyond the region, the portfolios are invested in a few other areas which we believe will continue to benefit from the tailwinds from several ongoing megatrends (see Figure 2).

For example, AI and associated infrastructure is set to “ride the wave” over the next few years with greater adoption rates, as well as the build-out of data-centres – which may further boost spending. Another trend is the “survival of the fittest” idea. Over the last few years with Covid, high interest rates, and robust competition (especially in the US), many industries have been impacted with companies consolidating. This has resulted in gains in market share, for the stronger players especially by leaders who are in firmer financial positions, to take advantage of sustained customer demand.

Figure 2: Fullerton’s key investment trends

Source: Fullerton Fund Management, October 2024.

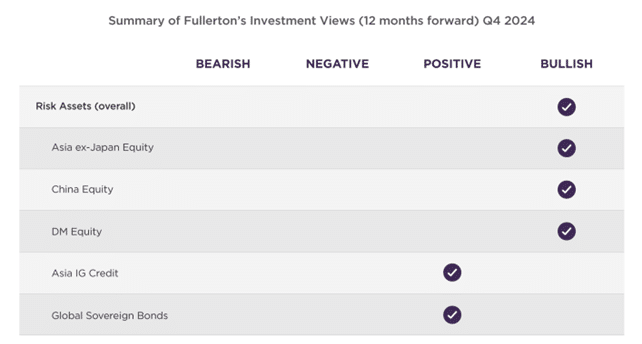

Figure 3: Fullerton’s investment outlook – bullish on Asia and Global Equities

Source: Fullerton Fund Management, October 2024. Views may be subject to change without prior notice.

1 See the Business Times (September 2024).

2 For further details on some of China’s monetary policy actions, see Reuters (September 2024).

3 Bloomberg, October 2024.

Important Information

No offer or invitation is considered to be made if such offer is not authorised or permitted. This is not the basis for any contract to deal in any security or instrument, or for Fullerton Fund Management Company Ltd (UEN: 200312672W) (“Fullerton”) or its affiliates to enter into or arrange any type of transaction. Any investments made are not obligations of, deposits in, or guaranteed by Fullerton. The contents herein may be amended without notice. Fullerton, its affiliates and their directors and employees, do not accept any liability from the use of this publication. The information contained herein has been obtained from sources believed to be reliable but has not been independently verified, although Fullerton Fund Management Company Ltd. (UEN: 200312672W) (“Fullerton”) believes it to be fair and not misleading. Such information is solely indicative and may be subject to modification from time to time.

Neither MSCI nor any other party involved in or related to compiling, computing or creating the MSCI data makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such data. Without limiting any of the foregoing, in no event shall MSCI, any of its affiliates or any third party involved in or related to compiling, computing or creating the data have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages. No further distribution or dissemination of the MSCI data is permitted without MSCI’s express written consent.

The audio(s) have been generated by an AI app