Executive summary

- Former President Trump returns to the White House and the Republican party takes power in both the executive and legislative branch of government.

- The incoming Trump administration’s policies may have a neutral effect on the US budget deficit and inflation.

- Higher import tariffs may be on the table, but this may not be as stressful as previously feared due to changing US consumption habits.

- Trade tensions with the US may lead to falling China export trade share with the US, but rising export trade share with Asia and a stable export trade share with the rest of the world.

- US household balance sheets remain robust, financial wealth is high, and unemployment is low.

- The decisive US election outcome removes immediate uncertainty and volatility, which is possibly what is driving a near-term rebound in risk assets.

A shocking outcome for investors because the polls were completely wrong

On 31 Oct, an average of US national polls had current Vice President Kamala Harris at 48.1% support versus Donald Trump at 46.7%1 – but on election day President-elect Trump’s share of the national vote surged to 51%. In his victory speech2 he made special mention that 5 Nov marked a historic “coming together” for “young, old, rural, urban, men, women, Asian-Americans, Arab-Americans, Latinos, all races and all citizens”.

Less surprising was the Democrats losing control of the Senate as their existing 1-seat majority was driven by Independents in their caucus – the 2024 election count suggests the Republicans may now hold 52 of the 100 seats (results for the House of Representatives are not finalised but it looks like the Republican majority will be extended by 4 seats)3 .

President-Elect Trump’s key policies need not worsen the US budget deficit and create inflation

Over the campaign, Donald Trump signalled that he would preserve (his) existing low tax rates4 beyond their statutory 31 Dec 2025 expiry, so their drag (assuming all else constant) would not impact fiscal account assumptions until 2026. Trump has also said he would seek a comprehensive review of the US tax system with the goal to make it more “adjustable” across corporates, income earners, and social security5. This encompasses many moving parts and any adjustments to thresholds, coverage, or statutory rates can potentially broaden government revenues, but with lower burdens on some sectors.

In his Presidential victory speech Donald Trump stressed “we will lower government debt and cut taxes”6. This is not as far-fetched as some investors may imagine – it has actually been the US experience over the years since the big tax cuts. US government debt has fallen from its record-high 133% to 120% of GDP (as at Q2 24) with the fiscal deficit also improving from 7.7% (Q2 23) to 6% of GDP (as at Q2 24) against the backdrop of very low statutory tax rates (especially for corporates)7. A key reason the US budget deficit has been slowly grinding lower, despite significant debt servicing costs, is because robust GDP growth is boosting government revenues while spending (as a percent of GDP) is relatively stable. This trend could continue in 2025 if US growth holds-up as the Consensus expects.

The prospect of higher US import tariffs may not be as stressful as many investors fear

The biggest surprise from Trump’s victory speech was no mention at all of the prospect of additional tariffs on US imports. Conspiracy buffs may conclude they can now be removed from the agenda because the rhetoric has won the Republicans office. We have presented compelling evidence in our Q4 24 Fullerton Investment Views that higher tariffs may not be as stressful as many investors fear.

As China is defending its global trade share, gaining share in Asia, has rising export prices, and is competitive

Under the current trade war, China’s export share to the US has fallen dramatically from its 25% (peak) to 14%. But at the same time, China’s global trade share has held stable (at 14%) and is creeping-up to Asia (at 14.2%)8. Asia (ex-China) has also enjoyed a rising trade share to the US. A simplistic push-back is China is just slashing prices to defend its export share in other markets. Some firms may be cutting prices, but on aggregate China’s export prices are rising, which is positive, and this is better than selling at home, as producer output prices are falling.

Based on real exchange rates, China is also very competitive – on par with South Korea, and second only to Japan globally. China also has significant market share (i.e. 15% or more) in global high-tech (high value) industries, notably transport (rail and sea) equipment, IT, and materials9.

US households do suffer as they pay more for the “must-haves” from China. But the US consumer is also buying a lot fewer other goods from China at the same time (replaced by alternative suppliers). On aggregate, the US household sector is robust: consumption as a share of GDP is rising again (Q3 24), household financial wealth (to income) is extremely high, unemployment is low, Personal Consumption Expenditure (PCE) inflation is back at 2.1% (Sep), and US goods prices are falling significantly (seeing deflation at minus 1.2%YoY in Sep).

Higher US tariffs on its “global” imports may also be unlikely

For President Trump to consider imposing tariffs on “all US imports” it would likely create vast US / cross-country legality hurdles, given the structure of the USMCA (2020) and select FTAs (covering many key markets across Latin America as well). Further, some Republicans, especially across the “rust-belt” States, may not agree to such policy proposals because they regard “free” trade with the Americas as vital for the supply of key raw materials supporting US manufacturing and jobs.

Implications for portfolio positioning10 – investors’ hate volatility and puzzling moves

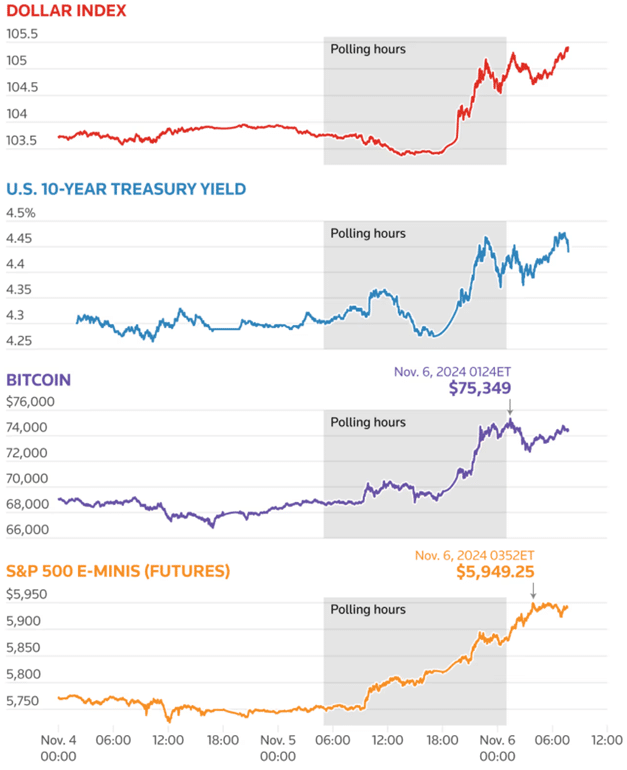

What is making investors very uncomfortable is how risk asset markets have behaved since the shock US election results (see Figure 1). US equities surged which could be as simple as investors now knowing that President Trump is in the position to make “America great again”. However, yields have also increased significantly, and that is a key concern if it reflects fears that US fiscal policy will become inflationary, or that the deficit will deteriorate significantly next year.

However, the surge in US yields could also be explained by investors being more bullish on US equities, and switching out of bonds. We know from recent global fund manager surveys (e.g BoA GFMS 15 Oct) that since mid-Oct overweights in global equity have tended to increase while bonds have flicked toward underweight. More importantly, the US household sector in aggregate continues to reduce its fixed income allocation (from a high level) as its equity allocation continues toward all-time highs.

The US dollar may be a key signpost

If the surge in bond yields is dominated by fears of higher US inflation or a worse fiscal deficit, then the US dollar should have fallen because of inflation-driven weaker purchasing power and public debt worries. Alternatively, and more compelling – higher yields, higher equities, and a stronger US dollar can collectively reflect stronger expectations of greater and sustained “US exceptionalism” – a theme from our Q4 24 Fullerton Investment Views. At 13.2% in Q2 2024, US all-company profitability is now tracking around the third highest ever. The two top peaks have been in this cycle, and the last 13% reading was back in Q4 195011. Such productivity-driven strength is appearing across Main Street (i.e. a population of around 6.1 million US employee firms) and not just Wall Street.

We need to keep monitoring developments closely

As investors we need to continue to try and be as forward-looking as we can, then distinguish between political rhetoric and potential policy directions. President Trump has always said “inflation is killing us” – that means he does not want high yields because that increases business costs, and in the same vein – he does not want a weak US dollar (because that increases imported inflation).

Donald Trump also talked of lower effective tax burdens for fossil-fuel linked industries (potentially funded by higher relative taxes on renewables). This could be expected to add to US dollar strength over time as the US is a net oil exporter. The policy could also support some US energy-linked equities (with robust balance sheets) at the expense of more strongly driven ESG-equities.

Overall we maintain our assessment that the policy initiatives that will be ultimately passed in 2025 can prove to be deficit and inflation neutral. We do not foresee our bullish outlook on US equities being derailed, by the actions of politicians, because the core fundamentals driving earnings are very supportive (i.e. above trend growth, robust productivity, very low real production costs, sustained consumer spending, and the Fed’s rate cuts).

Figure 1: US market reactions: US dollar appreciates, equities surge, yields higher

Source: LSEG and Reuters 6 Nov 2024. All times ET as at 0745

1 Reuters News and CNN (31 Oct 2024)

2 Fox 9 News 6 Nov 2024

3 NBC News 6 Nov 2024

4 The so-called ‘Trump tax cuts’, under the Tax Cuts and Jobs Act (2017), with impacts from 2018.

5 CBS News 5 Nov 2024

6 Fox 9 News 6 Nov 2024

7 Source: LSEG data

8 Source: LSEG trade share data

9 Source: LSEG data (to 2023/latest available).

10 Also refer to our background investment research on the US 2024 elections: the ‘flagship’ at the start of the year, which outlined possible sector level impacts, and illustrated the importance of fundamentals trumping politics (with respect to market returns) https://www.fullertonfund.com/fullerton-insights/2024-us-elections-and-potential-investment-implications/ Since then, in each quarterly Fullerton Investment Views (FIV), we have updated any key election-related issues i.e. pages 4-5 in https://www.fullertonfund.com/wp-content/uploads/2024/08/FIV-Q3-2024_Final-C.pdf and in our latest Q4 FIV (pp5, and pp11-12) Fullerton-Investment-Views-Q4-2024_FINAL.pdf

11 Source: LSEG Datastream, Nov 2024.

Important Information

No offer or invitation is considered to be made if such offer is not authorised or permitted. This is not the basis for any contract to deal in any security or instrument, or for Fullerton Fund Management Company Ltd (UEN: 200312672W) (“Fullerton”) or its affiliates to enter into or arrange any type of transaction. Any investments made are not obligations of, deposits in, or guaranteed by Fullerton. The contents herein may be amended without notice. Fullerton, its affiliates and their directors and employees, do not accept any liability from the use of this publication. The information contained herein has been obtained from sources believed to be reliable but has not been independently verified, although Fullerton Fund Management Company Ltd. (UEN: 200312672W) (“Fullerton”) believes it to be fair and not misleading. Such information is solely indicative and may be subject to modification from time to time.

The audio(s) have been generated by an AI app