Executive summary

- After a prolonged period of elevated Fed Funds rate, the FOMC commenced its easing action with a 50-bps rate cut in September 2024.

- Latest inflation readings, with PCE inflation falling back towards the Fed’s 2% target, provides sufficient justification for the policy rate reduction.

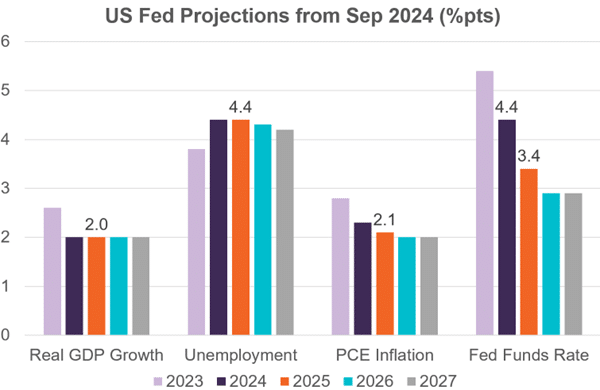

- The Fed has signalled that the policy rate can be trimmed to 3.4% in 2025.

- A sustained easing path over time can be broadly positive for risk assets – fixed income, corporate credits, and equities (with growth having an edge over value).

- USD weakness could accelerate.

The US Fed commences its big easing cycle against a backdrop of strong fundamentals

The Fed reduced the Fed Funds rate by 50bps from its policy target band of 5.25-5.50% at its 18 September meeting. The Fed endorsed the latest inflation indicators suggesting it is close to the 2% target; maintained its robust US growth outlook; and signalled that the policy rate can be cut to 3.4% in 2025 (i.e. just 50bps above the Fed’s 2.9% neutral policy rate assumption).

The Fed has almost achieved its dual mandate: inflation is tracking to 2% and extremely low unemployment is rising back toward full-employment assumptions

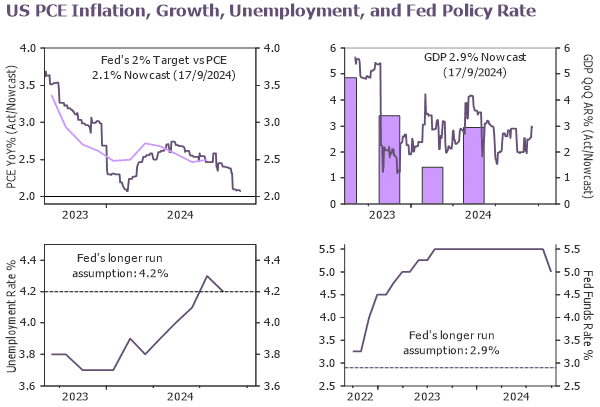

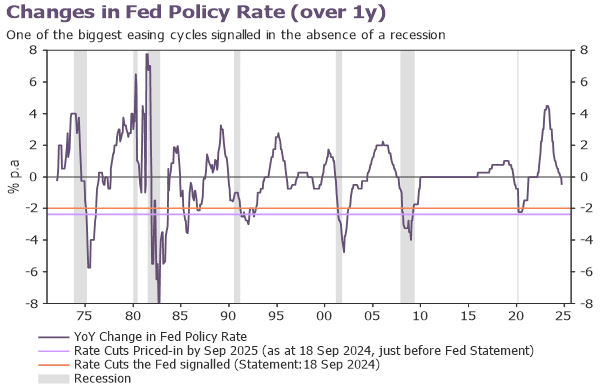

US GDP growth is tracking strongly and the latest nowcast for PCE inflation signals that it is almost back at the Fed’s 2% target (see Figure 1). The unemployment rate is rising from its exceptional low to levels more consistent with full-employment assumptions. It is therefore not surprising that the Fed has signalled that the policy rate can fall back significantly in 2025 (see Figure 2). In fact, given how inflation has surprised on the downside, and as unemployment is rising, there is a significant chance that the Fed will cut rates faster than it has signalled in 2025 to get back to neutral (a view which aligned with forward-market pricing before and after the Fed’s Statement. See Figure 3).

Figure 1: The Fed has almost achieved its dual mandate: 2% inflation and full-employment

Source: LSEG Datastream, September 2024.

Figure 2: The Fed expects robust US growth, contained unemployment, and low inflation

Source: FOMC, 18 September 2024.

Figure 3: The Fed commences its big easing against a backdrop of strong growth

Source: LSEG Datastream, September 2024.

Potential investment implications:

The positive environment for US equities and bonds can continue

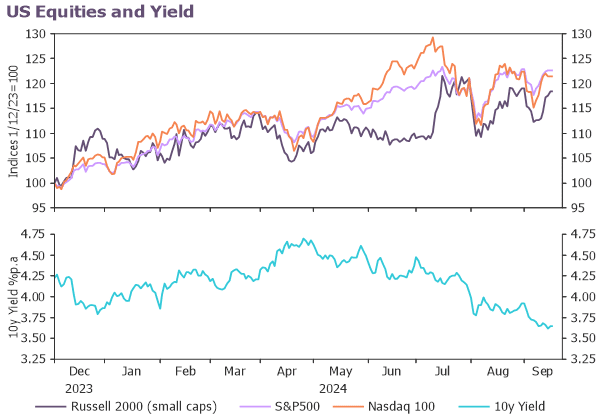

Falls in the Fed policy rate back toward the neighbourhood of neutral in 2025 should be supportive for liquidity, investor confidence, and US equity returns (see Figure 4). Returns are tracking strongly, expected earnings growth has just past its peak, and so the easing cycle, coupled with US GDP growth holding around trend, should ensure any slowdown remains gradual. As the yield curve is likely to slowly steepen and normalise over time this can be positive for interest rate-sensitive equity sectors in particular, such as financials. The US 10y yield could slip further as the Fed cuts rates which can create capital gains for bond investors. US corporate credit should also continue to perform well as growth holds-up, but investors should remain selective as the easing cycle may place further upward pressure on valuations.

Figure 4: The environment can remain positive for US equity and bond returns

Source: LSEG Datastream, September 2024.

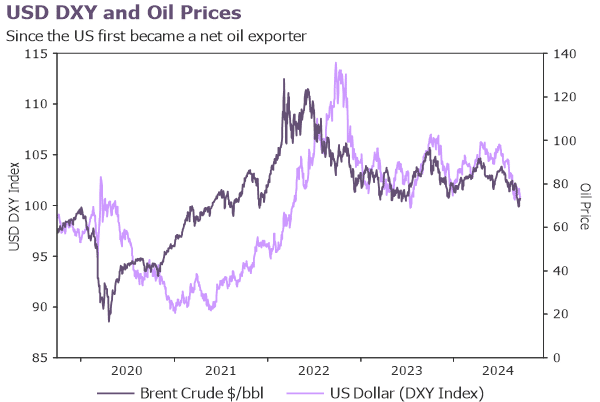

More headwinds are possible for the US dollar

Changes in the 10y yield differential for the US dollar (versus the six Developed Market countries within the DXY US dollar index), were already becoming less supportive, and the Fed’s easing cycle may add to the downward pressures. That said, what may moderate US dollar depreciation over time is the ECB’s rate cutting cycle which will defend some of the US dollar’s favourable carry. The other key factor that has been pulling the US dollar down is weak oil prices (see Figure 5). Oil prices are struggling because of weak demand expectations, especially from China. As the US is now a net oil exporter, the US dollar tends to depreciate when oil prices fall.

Figure 5: Beyond any Fed actions the USD faces headwinds from weak oil prices

Source: LSEG Datastream, September 2024.

A weaker US dollar, combined with a lower US 10y yield, can be positive for gold prices and Asia ex Japan equities (especially as the region benefits from US demand growth holding-up). Asia ex Japan equities are also likely to benefit from the significant increase in earnings growth expectations and we maintain our one-year ahead positive outlook.

Returns from cash are likely to ease further

As the Fed’s rate cuts unfold, returns from cash are likely to slow over time, but the asset class may achieve a “soft-landing” because of elevated global geopolitical risks. Lower US cash rates will mean that Singapore deposit rates will likely slip, but the pace of pass-through may be variable as the Singapore market has already moved significantly and the Monetary Authority of Singapore’s exchange rate policy will ultimately dictate where interest rates settle. Cash still plays an important role in one’s portfolio for liquidity, diversification, as well as holistic portfolio management and wealth planning purposes.

Important Information

No offer or invitation is considered to be made if such offer is not authorised or permitted. This is not the basis for any contract to deal in any security or instrument, or for Fullerton Fund Management Company Ltd (UEN: 200312672W) (“Fullerton”) or its affiliates to enter into or arrange any type of transaction. Any investments made are not obligations of, deposits in, or guaranteed by Fullerton. The contents herein may be amended without notice. Fullerton, its affiliates and their directors and employees, do not accept any liability from the use of this publication. The information contained herein has been obtained from sources believed to be reliable but has not been independently verified, although Fullerton Fund Management Company Ltd. (UEN: 200312672W) (“Fullerton”) believes it to be fair and not misleading. Such information is solely indicative and may be subject to modification from time to time.

The audio(s) have been generated by an AI app